16 April 2021

So much for the Brexit scare stories

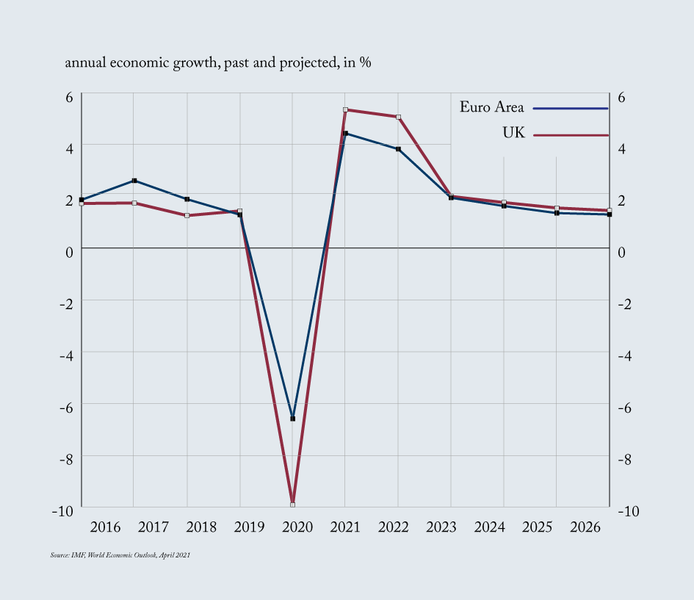

The collapse in UK-EU trade after January 1 was widely reported. What has not been reported nearly as much is that UK exports are bouncing back. They were up 46.6% in February after falling by 42% in January. Imports are not there yet. They were up 7.3% in February after a fall of 29.7% in January. The one prediction I am happy to make is that they will recover too. What these and other numbers are telling us is that even this bit of the Brexit scare stories will not come true. If you look at the latest IMF data and projections in the graphic above, you don't find a discernible macroeconomic effect of Brexit in the first ten years after the referendum. UK growth fell by more last year than eurozone growth, but this will be offset by higher growth this year. The future prosperity of the UK will depend to a large extent on the future policies of the UK government - Brexit or no Brexit.

The mistaken Brexit forecasts reflect three separate but overlapping phenomena. The first is political capture by official forecasters. The UK Treasury and the Bank of England were, of course, not neutral players. International institutions, like the IMF and the OECD, have the UK government among their shareholders.

A second group got it wrong because they allowed their political preferences to take over their economic judgments. That's most of the others. Brexit has been the most emotional policy dispute in recent times. It drove some people to insanity. I know very few people who are were genuinely neutral. Almost everyone's expectation of the economic effects correlated 100% with their political beliefs.

A third group, largely economists, got it wrong because they relied on bad models. There was an overlap of that group with the first and second group, but this one is worth identifying separately. I am talking about models based on long-term trade flows. As Brexit introduces a small degree of friction into physical goods trade, and quite a lot more friction into financial services and agricultural trade, these models predicted a long-term welfare loss. But these models are one-eyed. They only saw what might be lost.

Welcome to the widget school of economics. It is about things and containers, geography and manufacturing supply chains, the stuff of the 20th century economy. What it ignores is that events and technologies intrude. In the future, we will not only be trading different products, but an increasing proportion of trade will come in the form of data.

This is an area in which the UK could benefit from regulatory divergence from the EU. The EU’s business-unfriendly general data protection regulation inoculates it against artificial intelligence, which many Europeans regard as an American disease. Virus tracing apps, traffic-AI, face-recognition technology and military drones all depend on data sharing. With GDPR the EU gave itself a regime geared towards an analogue consumer in the pre-digital age.

We know that the US and China are the world's largest investors in AI. But those headline numbers are not telling the whole story. A report from the Centre for Data Innovation looking at qualitative criteria shows that the dynamics favour the US in particular. The US is leading on all the key criteria - talent, research, development, hardware, adoption and data - followed by China. The EU had some successes when it comes to the publication of academic papers, but is lagging behind both the US and China in all the other categories. The report concluded that Brexit would diminish the EU’s AI capability further.

Trade theories with their geographic proximity functions and notions of relative competitive advantage explain the flow of physical goods, but are irrelevant to data trade. The latter is already very important. The Progressive Policy Institute suggested that official statistics do not properly account for data trade. As it does not constitute an official category, it gets subsumed into services. So if you base your macro models on existing statistical categories, you are very likely to miss out on the single biggest economic growth area in global trade.

I am not making the argument that Brexit will be an economic success. I don't think it will. The best economic argument against Brexit is the one that was never made: that a UK government under either Labour or the Conservatives is unlikely to make best out of the opportunities for regulatory divergence.

The forecasts of unmitigated gloom, however, have been wrong and deceitful. When economists failed to predict the global financial crisis, they did not so out of malice or political bias. But their Brexit forecasts were not an innocent mistake - nor will they be remembered as such.

If you would like us to notify you when a new column appears, please fill out this form.